New Roof Depreciation Life

How Does Recoverable Depreciation Impact My Home Insurance Claim Valuepenguin Insurance Deductible Home Insurance Insurance Marketing

23 Items For Depreciation On Your Triple Net Lease Property Net Lease Tax Deductions Capital Gains Tax

What Is The Depreciation Of The Roof On A Commercial Building

Don T Pay For Depreciation Buying New Car New Cars Car

Section 179d Tax Deduction For Commercial Roof Replacements

Calculating Roof Depreciation In An Insurance Claim The Voss Law Firm P C

Correct normally these are either added to the basis or amortized over the life of a loan.

New roof depreciation life.

Pin On Articles Tips

Travel Trailer Depreciation What S My Travel Trailer Worth Rvblogger Travel Trailer New Travel Trailers Travel Trailer Hacks

Understanding Taxes Series Part 1 Depreciation Adventures In Cre

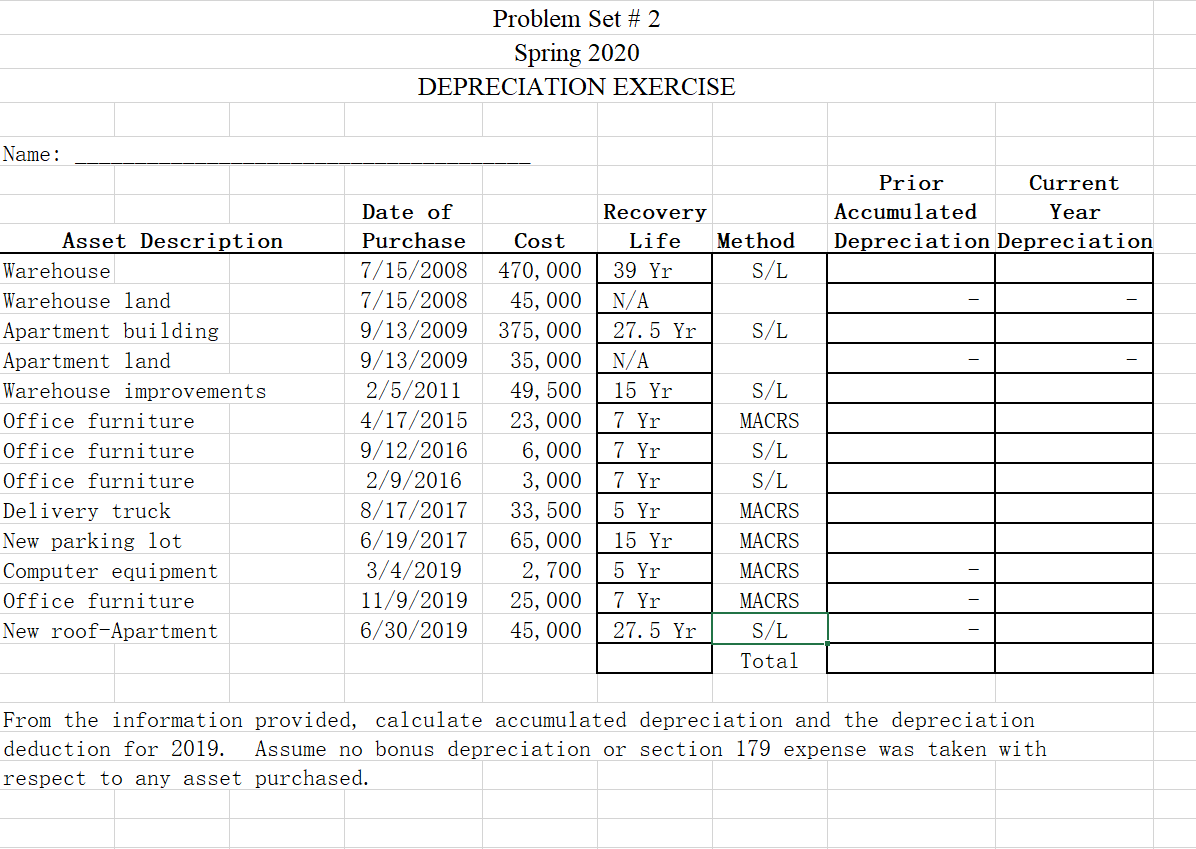

Problem Set 2 Spring 2020 Depreciation Exercise Chegg Com

Qualified Leasehold Improvement Property Depre Calculation

Rv Depreciation What You Can Expect With A New Rv Purchase Used Rvs Rv Life Rv Stuff

What Comes First The Property Or The Loan White Paint House House Painting Buying Property

Tax Depreciation Schedules Australia One Of The Least Benefit Of Property Depreciation Is That They Are Non Cash Deductions It Means Tax Deduction Legal Rule

Nonresidential Building Improvements Post 1993 Depre Calc

Roofing Tegola Master Everything On A Single Roof These Are The Characteristics Of Any Tegola Canadese Roof Quali Shingling Building Shingles Roof Shingles

Understanding Depreciation Recapture Taxes On Rental Property

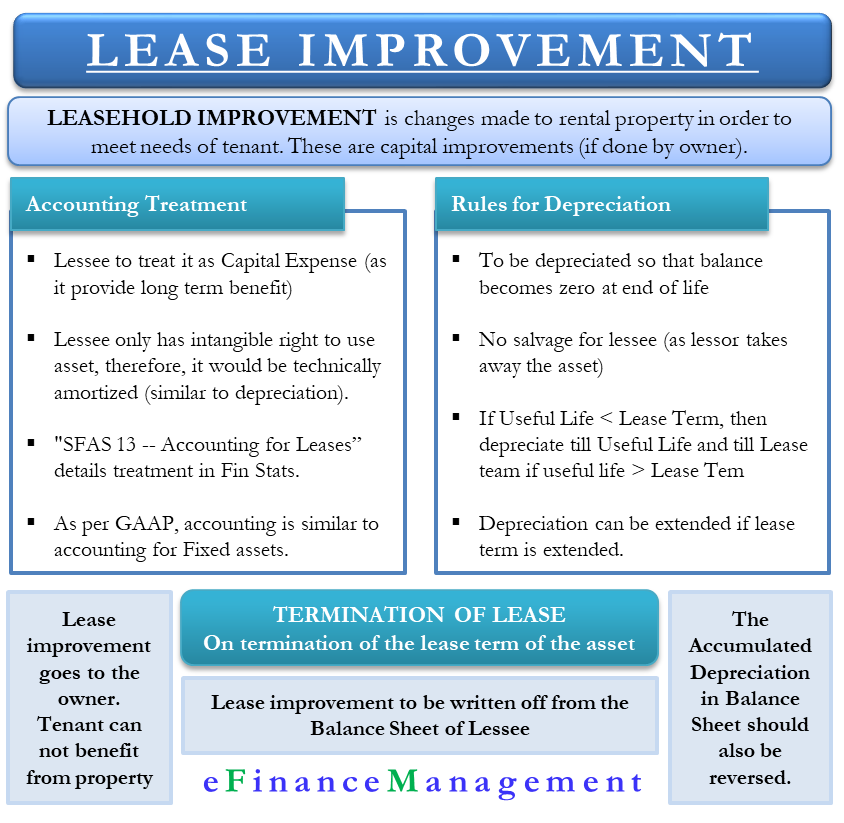

Leasehold Improvement Gaap Accounting Depreciation Write Off Efm

Prateek Grand City Bharosa Jyada Prateek Ka Vaada With Images Property Valuation Melbourne City

Roof Insurance Claim Process Questions Bob Behrends Roofing Gutters

Tokens Of Depreciation Instagram Tree House Outdoor

Home Based Business Jobs 2269 20180912135821 49 Home Office Tax Deduction Depreciation Recapture Rate 2016 Home Decor Pictures Home Decor Cool Landscapes

Accumulated Depreciation Meaning Accounting And More In 2020 Financial Management Accounting Principles Fixed Asset

The Dirt On Property Depreciation Property Investment Property Tax Time

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcqbzdn1pghydckmbdbwpdwee2usz7az1hlnbfbayb2inpgtdsev Usqp Cau

7 Ft Wide Lifetime Plastic Storage Sheds Are Available In 4 Lengths Robustly Built Their Steel Reinforced Fascia Panels Are Not Sus Plastic Storage Sheds Shed

Actual Cash Value The 15 Year Roof Rule Cw Roofing Construction

Pdf Download The Landlord S Financial Tool Kit Full Pages By Michael C Thomsett

Accounting For Equipment And Depreciation Self Progress Accounting Online Courses With Certificates Online Courses

Pittsburgh Plate Glass Sun Proof Paint 1926 Print Ad Drummer Mansion Roof Paint Print Ads Painting

Suprising Advice That Will Make Your Home Improvement Project Go Smoothly Home Improvement Projects Home Decor Shops Barn House Kits

Florida New Construction Rebate Program New Construction House Hunting Checklist Resources For Home Buyers Room Ideas Home Buying Tips Home Inspection

Best Rv Cover To Protect Your Roof With Images Rv Cover Rv Life Campervan Interior

Roofing Contract Template 145 Roofing Contract Contract Template Roofing

E Tax Depreciation Schedule Australia Will Be Australia S Driving Firm Who Give The Best Expense Devaluation Administrat Tax Investing Tax Deductions

Shibateen Blue Neighbourhood Life Is Strange Blue Sargent

Legalaccomplished Rental Property Tax Deductions Worksheet Rentalproperty

Strawbale Cottage I Like The Idea Of A Filled Bag Built To Shape For Above Door Easier Than What We Did Cob House Plans Straw Bale House Tiny House Cabin

At December 31 2020 Cord Company S Plant Asset And Accumulated Depreciation And Amortization Accounts Had Balances Homeworklib

Most Rv Roofs Will Develop A Leak Over Time Roof Leaks Damage The Structure Of Your Rv And Create Mold Over Time This Leads To Costly Rv

Rustic Porches Rustic Front Porch With A Cathedral Ceiling Provides A Dramatic Rustic Porch Screened Porch Designs Rustic Front Porch

Buyer Contact Form Black Real Estate Forms Realtor Forms Real Estate Agents Realtors Real Estate Marketing Active Real Estate In 2019 Real Estate Forms Real Estate Buyers Real Estate Investing

Https Www Scoremaine Org Wp Content Uploads 2018 11 Hiatt Msc Tax Cuts And Jobs Act Df 11 18 1 Pdf

Homeowners Insurance 101 Roof Age Matters At Claim Time

Tokens Of Depreciation Photo Urban Landscape Landscape

Going Solar Has Become Increasingly Affordable Thanks To Rebates Incentives And Financing Solar Energy Diy Solar Panels Solar Technology

Home Business Kuwait City 4604 20191125193313 49 Current Home Sales In My Area Wine Shop At Home Business In 2020 Story House Wine Shop At Home Best Home Business

Home Business Vpn 712 20180912123243 49 Best Home Business Ideas Philippines President Dut Remodeling Business Home Improvement Home Business Organization

Clayton Homes Of New Braunfels Tx Photos The Ponderosa A Gentleman S Ranch Home Rustic Clayton Homes Mobile Home Floor Plans Clayton Manufactured Homes

Want To Claim Taxdeductions Using Property Investment Recently The Australian Government Changed Legislation Weatherboard House Hamptons House Facade House

Source : pinterest.com